What is the Residential Energy Tax Credit?

What is the Residential Energy Tax Credit?

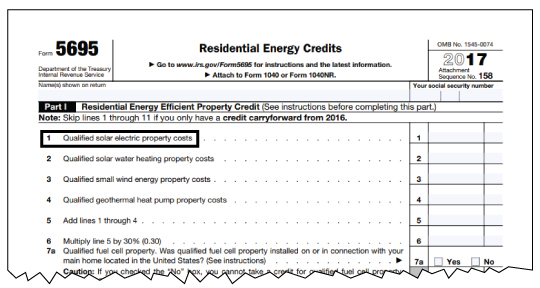

Currently, a taxpayer may claim a credit of 30% of qualified expenditures for a system that serves a dwelling unit located in the United States that is owned and used as a residence by the taxpayer. Expenditures with respect to the equipment are treated as made when the installation is completed. If the installation is at a new home, the “placed in service” date is the date of occupancy by the homeowner. Expenditures include labor costs for on-site preparation, assembly or original system installation, and for piping or wiring to interconnect a system to the home. If the federal tax credit exceeds tax liability, the excess amount may be carried forward to the succeeding taxable year.

How much is the Residential Energy Tax Credit?

- 30% for systems placed in service by 12/31/2019

- 26% for systems placed in service after 12/31/2019 and before 01/01/2021

- 22% for systems placed in service after 12/31/2020 and before 01/01/2022

- There is no maximum credit for systems placed in service after 2008.

- Systems must be placed in service on or after January 1, 2006, and on or before December 31, 2021.

- The home served by the system does not have to be the taxpayer’s principal residence.

How do I apply for the Residential Energy Tax Credit?

Applying for the Residential Energy Tax Credit is as simple as filling out IRS Form 5695.